Monthly Market Memorandum - February 2026

Contents

Executive Summary

Macro & Market Overview

2.1 Inflation & Rates

2.2 Global Economic Activity

2.3 Equity Markets

2.4 Fixed Income & Credit

2.5 Commodities & Alternatives

Key Themes of the Month

3.1 The Repricing of Global Growth Expectations

3.2 Diverging Regional Equity Performance

3.3 Credit Markets Continue to Price a Soft Landing

What to Watch Next Month

Closing Remarks

Executive Summary

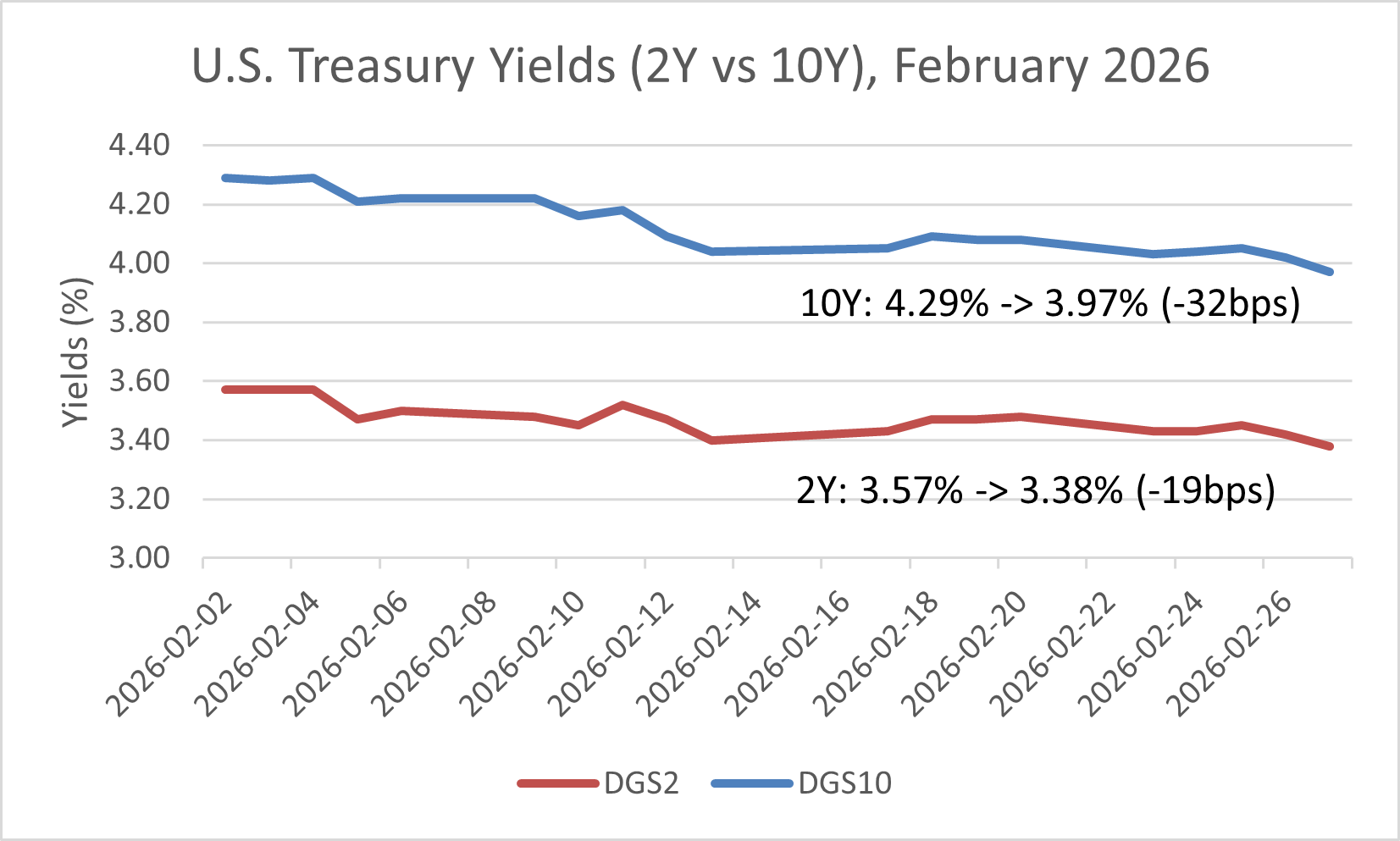

February 2026 markets shifted away from the higher yield narrative that defined January and instead moved toward a partial repricing of growth and policy expectations. Government bond yields declined across the curve during the month, signaling that markets began to price a slower pace of economic momentum and a greater likelihood that inflation pressures would continue easing. The 10 year U.S. Treasury yield fell more than the 2 year yield, indicating modest curve flattening as long term growth expectations softened.

Equity markets delivered mixed performance across regions. U.S. indices experienced modest declines after strong gains earlier in the year, while European equities showed relative resilience. This divergence reflected differences in economic momentum, sector composition, and investor positioning. Technology heavy U.S. benchmarks faced valuation pressure as interest rate expectations shifted, while European markets benefited from signs of stabilization in manufacturing activity.

Credit markets remained notably stable despite the shift in rates. Investment grade and high yield corporate spreads showed limited widening, indicating that investors continued to view corporate balance sheets as resilient and default risk as contained. The persistence of tight spreads suggested that financial conditions remained supportive even as macroeconomic uncertainty increased.

Commodity markets reflected a mixed macro environment. Oil prices moved with changing expectations around global demand and energy consumption, while gold remained supported by ongoing macro uncertainty and demand for defensive assets. The divergence between cyclical commodities and safe haven assets highlighted the market’s uncertain outlook for growth.

Three developments shaped the market environment entering March. First, falling bond yields signaled that markets were adjusting expectations for both growth and monetary policy. Second, global economic activity remained uneven, with manufacturing stabilizing in some regions while continuing to contract in others. Third, credit markets maintained confidence in corporate fundamentals, reinforcing the perception that the economic slowdown remained moderate rather than severe.

Taken together, February suggested a transition from the rate driven pressures of early 2026 toward a more balanced macro environment characterized by slower growth, easing inflation pressures, and continued investor demand for income generating assets.

Macro & Market Overview

Inflation & Rates

Inflation dynamics and interest rate expectations remained central to market behavior in February 2026. After several months of elevated yields and persistent inflation concerns, bond markets began to price a more balanced outlook for both inflation and economic growth. While inflation remained above central bank targets in most advanced economies, incoming data suggested that price pressures were moderating compared with late 2025.

In the United States, monetary policy expectations continued to evolve as investors reassessed the trajectory of both inflation and economic activity. Federal Reserve communications during the month emphasized data dependency, reinforcing the view that policy adjustments would remain gradual and responsive to incoming economic indicators rather than following a predetermined path.

Against this backdrop, Treasury yields declined across the curve during February. The 10 year yield fell more than the 2 year yield, indicating that markets were adjusting expectations for long term growth and inflation. This movement produced modest flattening in the yield curve, reflecting a balance between easing inflation concerns and continued uncertainty around economic momentum.

Figure 1. Daily U.S. Treasury yields during February 2026. Both short and long maturity yields declined during the month, with the 10 year yield falling more than the 2 year yield, indicating modest curve flattening as markets adjusted expectations for inflation and monetary policy.

The decline in yields had several implications for financial markets. Lower long term rates reduced valuation pressure on interest rate sensitive sectors such as technology and real estate, while also improving conditions for fixed income investors who had faced persistent duration losses earlier in the cycle. At the same time, the continued inversion of the yield curve highlighted lingering concerns about medium term economic growth.

Outside the United States, bond markets reflected similar dynamics. European government bond yields declined modestly as inflation indicators softened and economic growth remained subdued. In Japan, yields remained relatively stable as the Bank of Japan maintained its gradual approach toward policy normalization.

Overall, February reinforced that bond markets remained highly sensitive to shifts in inflation expectations and growth data. Even modest changes in economic indicators produced noticeable movements in yields, reflecting the central role of monetary policy expectations in shaping global asset prices.

-

Sources:

U.S. Treasury Yield Data

https://fred.stlouisfed.org/series/DGS10

U.S. Treasury Yield Data

https://fred.stlouisfed.org/series/DGS2

Federal Reserve Monetary Policy Statements

Global Economic Activity

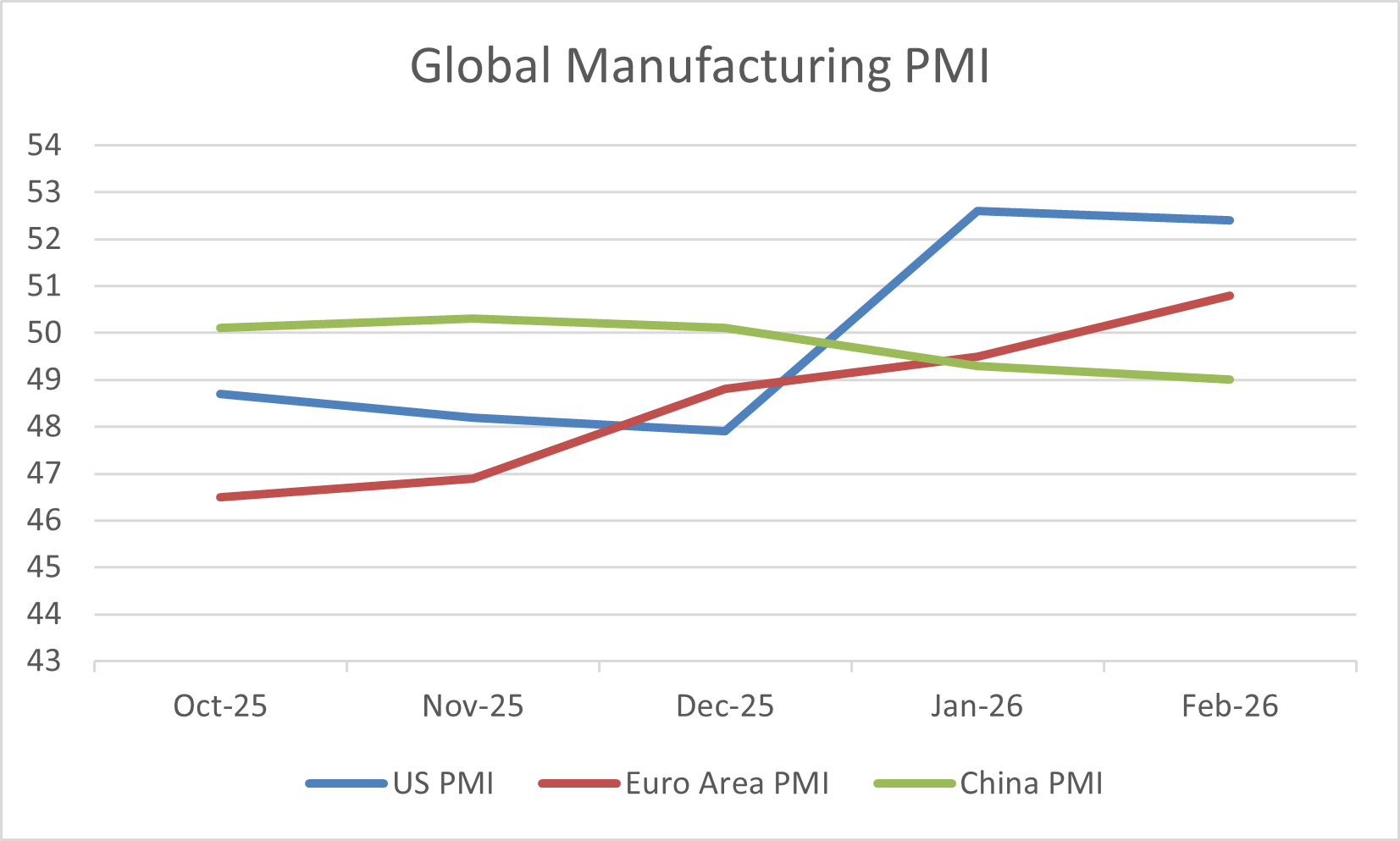

Global economic activity in early 2026 continued to display uneven momentum across major regions. While service sector activity remained relatively resilient, manufacturing indicators provided a more cautious signal about global growth. Purchasing managers’ indices across several major economies suggested that industrial activity remained weak despite tentative signs of stabilization.

In the United States, manufacturing conditions improved modestly compared with late 2025. The ISM Manufacturing PMI moved back into expansion territory, indicating stronger new orders and production activity. However, the recovery remained uneven across sectors, with durable goods production showing more resilience than export oriented industries.

In Europe, economic momentum remained fragile but showed early signs of stabilization. Manufacturing PMI readings approached the expansion threshold after several months of contraction, suggesting that industrial activity may have reached a cyclical trough. Nevertheless, structural challenges including weaker global trade and higher financing costs continued to constrain the pace of recovery.

China’s manufacturing sector remained under pressure. Official PMI readings stayed below the expansion threshold, reflecting ongoing weakness in property related industries and cautious domestic demand. While targeted policy support and infrastructure spending provided some stabilization, broader industrial momentum remained limited.

Figure 2. Manufacturing purchasing managers’ indices across major economies. PMI readings above 50 indicate expansion in manufacturing activity while readings below 50 signal contraction.

Japan’s manufacturing sector showed similar dynamics, with activity fluctuating around the contraction threshold. Currency volatility and rising input costs continued to influence production decisions, while external demand remained a key determinant of industrial output.

Taken together, global manufacturing indicators suggested that the world economy remained in a low growth environment. Stabilization in some regions contrasted with ongoing contraction in others, reinforcing the theme of uneven economic momentum across the global economy.

-

ISM Manufacturing PMI

S&P Global PMI Data

China Manufacturing PMI

Equity Markets

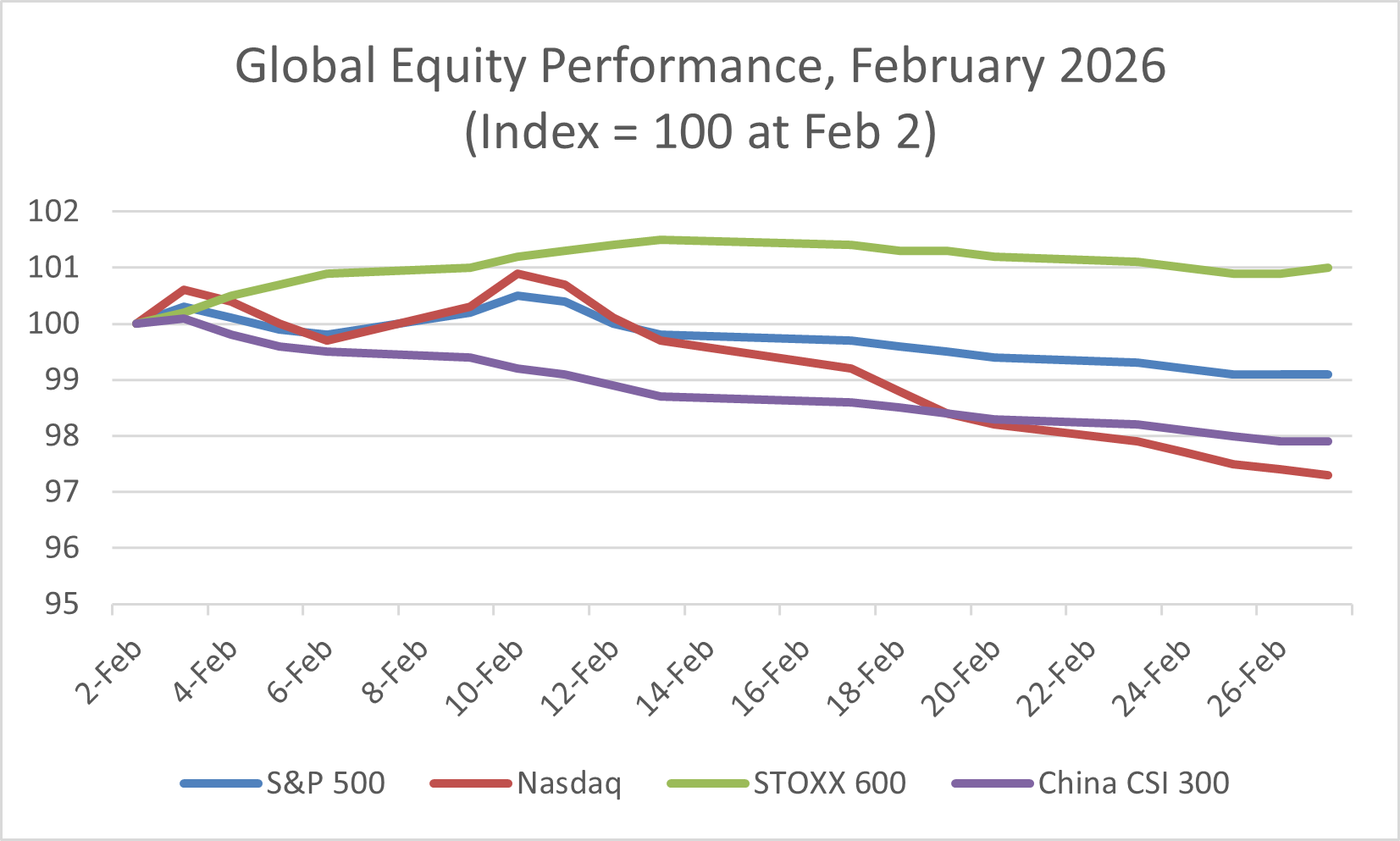

Global equity markets delivered mixed performance during February 2026 as investors reassessed both economic momentum and interest rate expectations. Following strong gains earlier in the year, U.S. equity benchmarks experienced modest declines during the month. Valuation pressures linked to interest rates and shifting growth expectations contributed to weaker performance among technology and growth oriented sectors.

The S&P 500 and Nasdaq Composite both declined modestly over the month. Technology stocks in particular faced greater sensitivity to changing interest rate expectations due to their reliance on longer duration earnings growth. While corporate earnings remained broadly stable, investors displayed greater caution toward high valuation sectors.

European equities showed relative resilience compared with their U.S. counterparts. The STOXX Europe 600 posted modest gains during February as improving manufacturing indicators supported investor sentiment. Lower valuations relative to U.S. markets and stronger performance in cyclical sectors contributed to this outperformance.

Figure 3. Indexed performance of major global equity benchmarks during February 2026. U.S. equities declined modestly while European equities showed relative resilience and Chinese equities remained under pressure.

Chinese equity markets remained comparatively weak during the month. Ongoing property sector challenges, cautious consumer behavior, and uncertainty around policy effectiveness continued to weigh on investor sentiment. Although government support measures helped stabilize certain sectors, broader market participation remained limited.

Overall, February highlighted the divergence between regional equity markets. Differences in economic momentum, policy conditions, and sector composition continued to shape global equity performance, reinforcing the importance of regional diversification for investors.

-

S&P 500 Index Data

Nasdaq Composite Data

STOXX Europe 600 Index Data

CSI 300 Index Data

Fixed Income and Credit

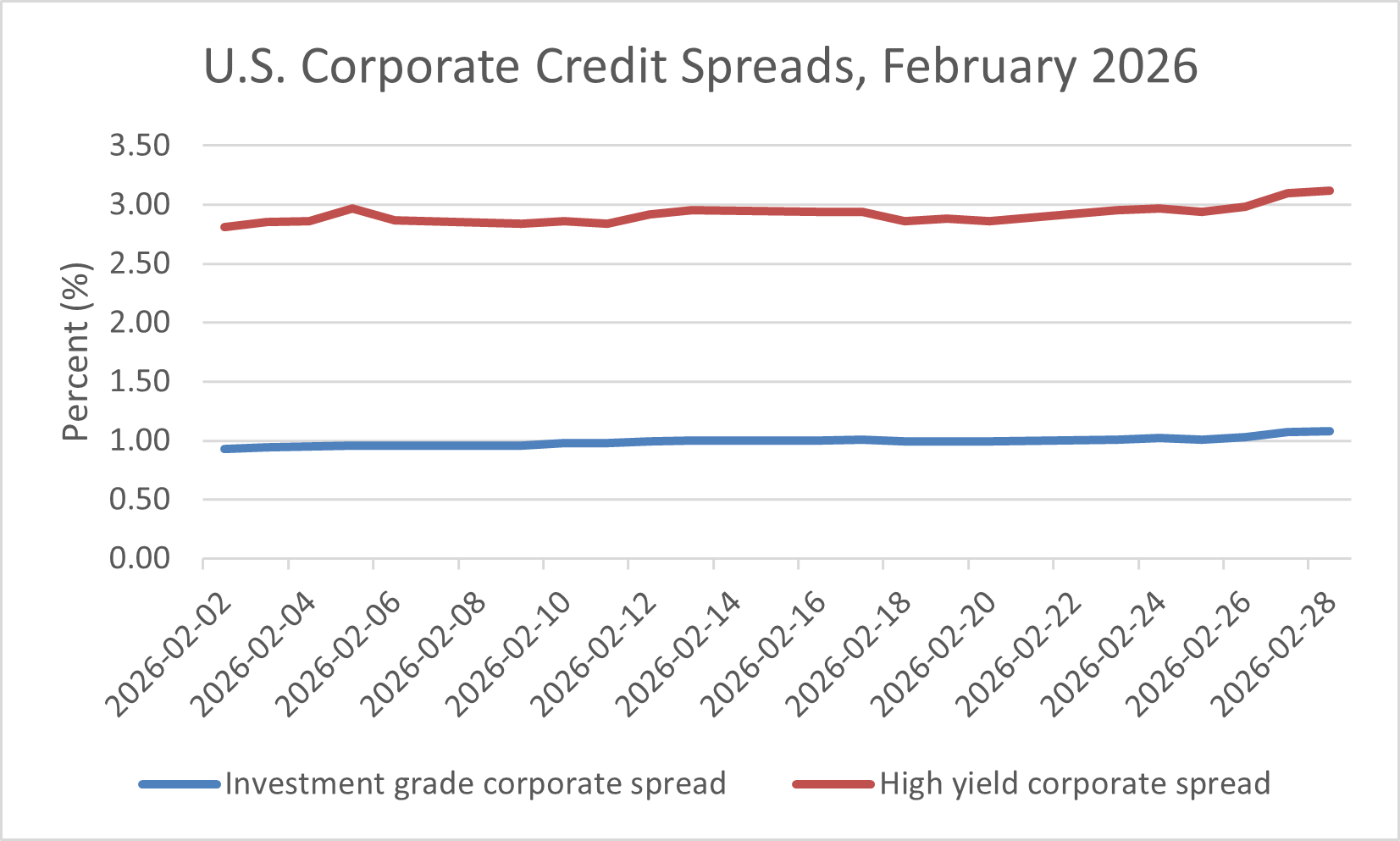

Fixed income markets in January 2026 reflected continued divergence between interest rate risk and credit risk. While short and long term government bond yields remained elevated, credit spreads stayed relatively tight, indicating that investors remained comfortable with corporate balance sheet risk. This separation reinforced the view that markets were more concerned about duration exposure than about near term default risk.

In the United States, Treasury yields showed modest upward pressure across the curve. The 2 year yield increased over the month, reflecting expectations that policy easing would remain gradual rather than rapid. The 10 year yield also moved higher, supported by persistent government bond supply and firm long term growth expectations. As a result, the yield curve remained relatively flat, with limited evidence of aggressive steepening or inversion. This environment continued to challenge long duration fixed income assets, as higher yields reduced bond prices and limited total returns.

Figure 4. U.S. investment grade and high yield option adjusted spreads during February 2026. Credit spreads remained relatively stable, indicating continued investor confidence in corporate balance sheets and manageable default risk.

The stability of credit spreads suggested that financial conditions remained supportive for corporate borrowers. Many companies had previously refinanced debt during periods of lower interest rates, reducing near term refinancing risk and improving balance sheet flexibility.

This resilience reinforced the view that the global economic slowdown remained moderate rather than severe. As long as employment conditions and corporate earnings remained stable, credit markets appeared comfortable maintaining relatively tight spreads despite broader macro uncertainty.

-

Investment Grade OAShttps://fred.stlouisfed.org/series/BAMLC0A4CBBB

High Yield OAShttps://fred.stlouisfed.org/series/BAMLH0A0HYM2

Commodities & Alternatives

Commodity markets in February reflected shifting expectations around global growth and macroeconomic uncertainty. Energy prices moved in response to evolving demand expectations, while precious metals continued to attract investor interest as defensive assets.

Oil prices fluctuated during the month as markets weighed competing forces. On one hand, slowing global manufacturing activity suggested weaker demand for energy. On the other hand, supply discipline from major producers and geopolitical developments continued to support prices. The resulting movement in oil prices reflected the balance between these opposing factors.

Gold prices remained comparatively stable during the month. Demand for safe haven assets persisted as investors navigated uncertainty around inflation, economic growth, and geopolitical developments. Gold also benefited from declining bond yields, which reduced the opportunity cost of holding non interest bearing assets.

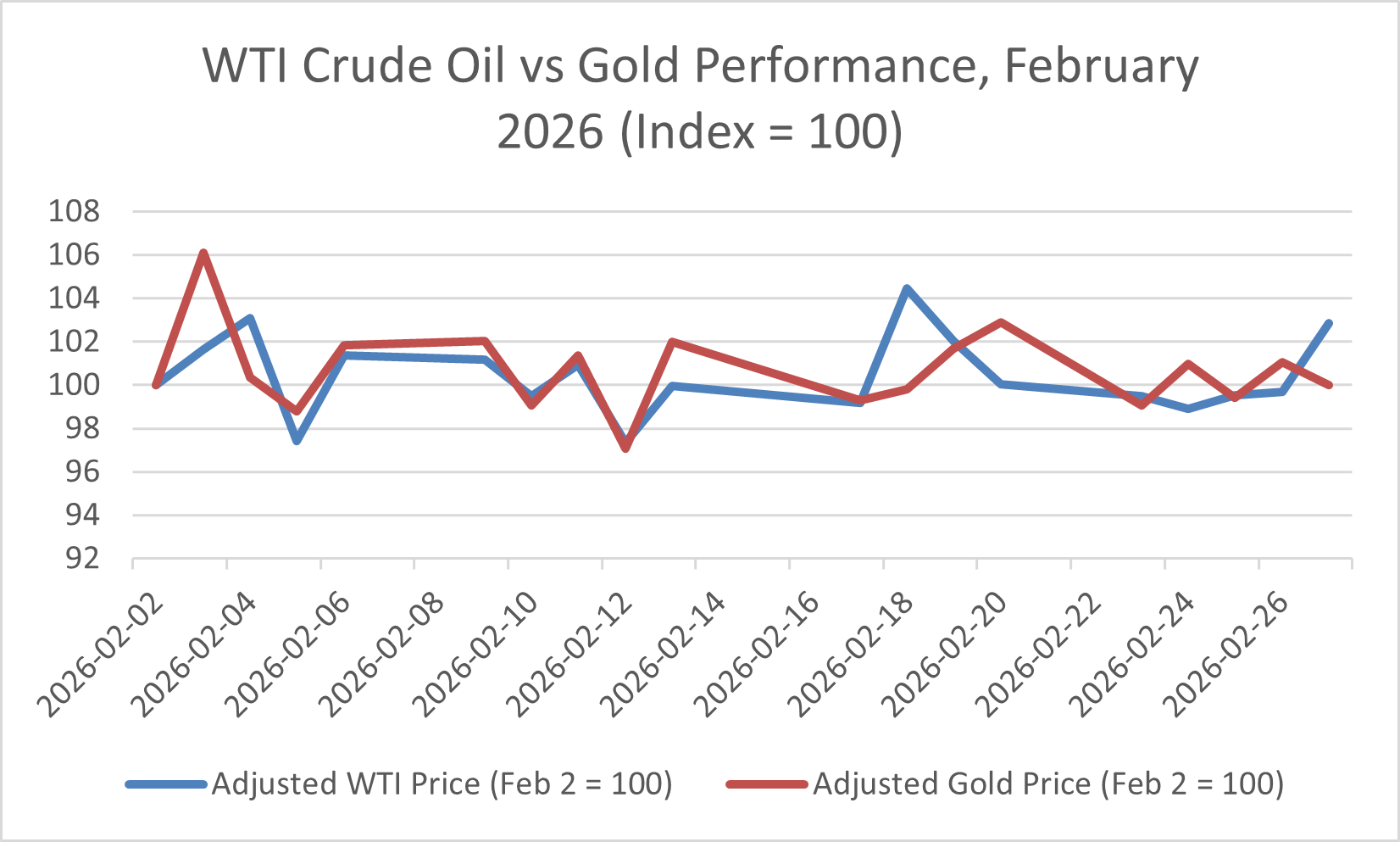

Figure 5. Indexed performance of WTI crude oil and gold during February 2026. Oil prices reflect expectations around global energy demand while gold performance captures shifts in safe haven demand and macroeconomic uncertainty.

Beyond traditional commodities, alternative assets continued to adjust to the evolving interest rate environment. Real assets such as infrastructure and commercial real estate remained sensitive to financing costs, while private market activity continued to emphasize income generation and capital preservation.

Overall, commodity markets reflected the broader macro environment of moderate growth and persistent uncertainty. Divergent movements between energy and precious metals highlighted the market’s mixed outlook for both economic activity and financial stability.

-

WTI Crude Oil Prices

https://fred.stlouisfed.org/series/DCOILWTICO

Gold Futures Prices

https://finance.yahoo.com/quote/GC=F/history

Commodity Market Data

Key Themes of the Month

Theme 1: The Repricing of Global Growth Expectations

Financial markets in February reflected a shift in expectations around global economic momentum. After entering the year with relatively strong market sentiment and elevated interest rates, investors began adjusting their outlook toward slower but still stable growth. Bond markets led this repricing, while commodity and macro indicators reinforced the perception that economic expansion remained uneven across regions.

Falling Long-Term Yields Signal Softer Growth Expectations

One of the clearest market signals during February came from government bond markets. Treasury yields declined across the curve during the month, with the 10 year yield falling more than the 2 year yield. This movement indicated that investors were reassessing long term growth expectations and adjusting their expectations for inflation and monetary policy.

As shown in Figure 1, both short and long maturity yields declined during February, although the decline was more pronounced in longer term yields. This modest flattening of the yield curve suggested that markets were beginning to price a slightly weaker growth outlook while still expecting monetary policy to remain relatively restrictive in the near term.

Several factors contributed to this repricing. Economic indicators pointed to moderating momentum in certain sectors of the economy, while inflation data continued to show gradual improvement compared with late 2025. At the same time, investors remained attentive to the potential for slower global demand and tighter financial conditions.

Global Manufacturing Stabilizes but Remains Uneven

Economic data released during February reinforced the perception that global growth remained uneven. Manufacturing indicators showed stabilization in several major economies but did not yet signal a broad recovery in industrial activity.

As shown in Figure 2, purchasing managers’ indices across major economies continued to diverge. In the United States, manufacturing activity returned to expansion territory, reflecting stronger new orders and production levels. In contrast, China’s manufacturing sector remained below the expansion threshold, indicating ongoing contraction in industrial output. European manufacturing indicators improved modestly and approached the expansion threshold, suggesting that the region may be emerging from a prolonged industrial slowdown.

This divergence reflected several structural differences between regions. The United States continued to benefit from strong domestic demand and resilient labor markets, while China faced persistent weakness in property related industries and cautious consumer behavior.

Commodity Markets Reflect Uncertain Demand Conditions

Commodity markets provided additional evidence of uncertainty around global demand. Energy prices fluctuated during the month as markets evaluated the balance between supply conditions and expectations for global economic activity.

Oil prices moved in response to changing expectations around industrial demand and energy consumption. Slower manufacturing growth in several regions raised concerns about future oil demand, while supply discipline among major producers helped limit downside pressure.

Gold prices showed a different dynamic. As illustrated in Figure 5, gold remained relatively well supported during February. Declining bond yields reduced the opportunity cost of holding non interest bearing assets, while persistent macro uncertainty continued to drive demand for safe haven assets.

The divergence between oil and gold highlighted the mixed outlook for global growth.

-

U.S. Treasury Yield Data

https://fred.stlouisfed.org/series/DGS10

U.S. Treasury Yield Data

https://fred.stlouisfed.org/series/DGS2

ISM Manufacturing PMI Report

https://www.ismworld.org/supply-management-news-and-reports/reports/ism-report-on-business/

Global Manufacturing PMI Releases

https://www.pmi.spglobal.com/Public/Release/PressReleases

China Manufacturing PMI Data

https://www.stats.gov.cn/english/

WTI Crude Oil Prices

https://fred.stlouisfed.org/series/DCOILWTICO

Gold Futures Historical Data

https://finance.yahoo.com/quote/GC=F/history

International Energy Agency Oil Market Report

Diverging Regional Equity Performance

Global equity markets displayed notable regional divergence during February. While overall market movements were relatively modest, performance differences between major regions reflected variations in economic momentum, sector composition, and investor positioning.

U.S. Equity Momentum Slows After Early-Year Gains

U.S. equity markets experienced a modest slowdown during February following strong gains earlier in the year. Major benchmarks such as the S&P 500 and Nasdaq Composite declined slightly during the month as investors reassessed valuations and interest rate expectations.

Technology and growth oriented sectors were particularly sensitive to these developments. Companies with longer duration earnings profiles remain more exposed to changes in interest rates because their valuations depend heavily on future cash flows.

As shown in Figure 3, U.S. equity indices underperformed several international benchmarks during the month.

European Equities Benefit from Industrial Stabilization

European equity markets displayed greater resilience during February. The STOXX Europe 600 index posted modest gains during the month as improving manufacturing indicators supported investor sentiment.

Stabilization in industrial activity helped support sectors that are more heavily represented in European markets, including industrials, materials, and financials. In addition, European equity valuations remained lower than their U.S. counterparts.

China Remains the Weak Link in Global Equity Markets

Chinese equity markets remained comparatively weak during February. Structural challenges including property sector weakness, cautious consumer spending, and ongoing policy uncertainty continued to weigh on investor sentiment.

Despite targeted stimulus measures and infrastructure investment, China’s economic recovery remained uneven.

-

S&P 500 Historical Data

https://finance.yahoo.com/quote/%5EGSPC/history

Nasdaq Composite Historical Data

https://finance.yahoo.com/quote/%5EIXIC/history

STOXX Europe 600 Index Data

CSI 300 Index Historical Data

https://finance.yahoo.com/quote/000300.SS

Eurozone Manufacturing PMI Releases

https://www.pmi.spglobal.com/Public/Release/PressReleases

People’s Bank of China Policy Announcements

Credit Markets Continue to Price a Soft Landing

Credit markets remained one of the most stable components of the global financial system during February. Despite shifting expectations around growth and interest rates, corporate bond spreads showed limited widening across both investment grade and high yield markets.

Credit Spreads Remain Near Cycle Lows

Corporate bond spreads remained relatively tight throughout February. Investment grade and high yield spreads fluctuated modestly but remained near historically low levels.

As shown in Figure 4, the stability of credit spreads indicated that investors continued to view corporate credit risk as manageable.

Elevated Base Rates Increase the Attractiveness of Carry

Higher policy rates increased the yield available on corporate bonds, allowing investors to generate attractive income without relying heavily on capital appreciation.

Corporate balance sheet strength also contributed to credit market stability. Many companies refinanced debt earlier in the cycle when borrowing costs were lower, extending maturity profiles and reducing near term refinancing risk.

-

ICE BofA US Corporate BBB Option-Adjusted Spreadhttps://fred.stlouisfed.org/series/BAMLC0A4CBBB

ICE BofA US High Yield Option-Adjusted Spreadhttps://fred.stlouisfed.org/series/BAMLH0A0HYM2

Federal Funds Effective Ratehttps://fred.stlouisfed.org/series/FEDFUNDS

Federal Reserve Financial Accounts of the United Stateshttps://www.federalreserve.gov/releases/z1/

Moody’s Corporate Default and Recovery Reporthttps://www.moodys.com/researchandratings

S&P Global Corporate Credit Outlookhttps://www.spglobal.com/ratings

What to Watch For Next Month

Looking ahead to March 2026, market direction will likely depend on how incoming economic data shapes expectations around growth, inflation, and monetary policy. February’s market movements suggested a moderation in economic momentum rather than a sharp downturn, but several key indicators will determine whether this narrative continues.

One of the most important developments to monitor will be upcoming inflation data in the United States and other major economies. Although inflation has eased compared with the peaks observed earlier in the cycle, core price pressures remain above central bank targets. If inflation continues to moderate, bond yields may remain contained and support valuations in interest rate sensitive sectors. Conversely, any renewed acceleration in inflation could reverse the decline in long term yields and reintroduce volatility into both equity and fixed income markets.

Labor market conditions will also play a central role in shaping market expectations. Employment growth and wage data provide critical insight into the underlying strength of consumer demand. A resilient labor market would support household spending and reinforce the view that the global economy is moving toward a soft landing. However, signs of weakening employment conditions could quickly shift sentiment toward concerns about a broader economic slowdown.

Corporate earnings will remain another key focus for investors. Although earnings growth has remained relatively stable across many sectors, markets are increasingly attentive to forward guidance from companies. If firms begin to signal slower revenue growth or declining margins, equity markets could face renewed pressure. In particular, the performance of large technology companies will remain important given their outsized influence on major U.S. equity indices.

Developments in China and Europe will also influence global growth expectations. Policy announcements, fiscal measures, or improvements in industrial activity could provide support to global demand. Conversely, continued weakness in manufacturing or property markets may reinforce the uneven growth environment that characterized February.

Finally, credit markets warrant close monitoring. Corporate bond spreads remained relatively tight throughout February, suggesting continued investor confidence in corporate balance sheets. However, if economic conditions deteriorate more rapidly than expected or corporate earnings weaken materially, credit markets may begin to reprice risk. Any widening in credit spreads could signal tightening financial conditions and increase volatility across asset classes.

Closing Remarks

February 2026 highlighted a market environment characterized by cautious adjustment rather than dramatic shifts in economic conditions. After entering the year with elevated interest rates and strong equity market performance, investors began reassessing expectations for growth, inflation, and monetary policy.

Bond markets led this adjustment, with Treasury yields declining across the curve as investors priced a more balanced outlook for economic activity. At the same time, global manufacturing data suggested that while industrial activity may be stabilizing in some regions, the broader global economy remains characterized by uneven growth.

Equity markets reflected this environment through regional divergence rather than broad based declines. U.S. equity indices experienced modest declines as valuations adjusted, while European markets showed greater resilience amid improving industrial indicators. Chinese equities continued to lag global peers, highlighting the ongoing structural challenges facing the country’s economy.

Perhaps most notably, credit markets remained remarkably stable throughout the month. Corporate bond spreads remained tight, signaling continued confidence in corporate balance sheets and reinforcing the perception that financial conditions remain supportive despite slower economic momentum.

Taken together, these developments suggest that markets remain positioned for a gradual economic adjustment rather than a sharp downturn. Investors appear increasingly focused on resilience, favoring assets with stable earnings, strong balance sheets, and reliable income streams.

As the global economy moves further into 2026, the interaction between inflation trends, monetary policy decisions, and global growth dynamics will continue to shape market performance. While uncertainty remains elevated, the stability of credit markets and the gradual moderation of inflation provide a foundation for a more balanced market environment in the months ahead.